Custom Search

|

|

|

|

|

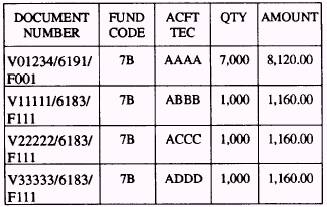

TRANSFERS BETWEEN SHIPS UNDER THE SAME TYCOM.- Transfers of DBOF (formerly NSF) type material between the same TYCOM is nonchargeable. The material transfers will be included in the B summary of the transferring ship or activity. This also covers transfers of TYCOM centrally procured material. This procedure does not include subsistence, ship's store stock, and resale clothing. TRANSFERS BETWEEN UNITS/FUNC-TIONS FUNDED BY DIFFERENT OPERATING BUDGETS.- Transfers of DBOF (formerly NSF) type material between ships of different TYCOM are chargeable transactions. The value of the material transfers will be included in the A summary of the transferring unit. This procedure does not include subsistence, ship's store stock, and resale clothing. APA MATERIAL TRANSFERS.- The inter-ship transfers of APA material are nonchargeable transactions that are not required to be summarized. However, these transactions are required to be documented and a copy retained in file as proof of transfer. TRANSFER OF PETROLEUM PROD-UCTS.- Fund code UZ is used by SAC 207 activities for requisitioning or purchasing aviation fuels. When the transaction is processed, it will appear in the appropriate Financial Inventory Report (FIR) caption. The value of materials received for stock from other supply officers are processed as FIR caption F4. The receipts from procurement (commercial activities) will be processed as FIR caption A1. The transferring activity will show the transaction in FIR caption P4 (transfer to other supply officer-stock). Transfer of fuels from SAC 207 stock to ship's own use or other ship's propulsion or power generation will be charged to the fleet commander's centrally managed allotment. Transfer of fuels and lubricants from SAC 207 ships for use in ship's vehicles ashore is processed as an issue and charged to the ship's OPTAR. Issues to Aviation Units by Aviation Ships.- Issue of aviation fuels by SAC 207 activities to support squadrons is normally conducted on DD Form 1348 (6-pt). The requisition will cite the squadron's fund code (for example 7B) that will be charged for the fuel issue. The SAC 207 issuing ship will process the transaction on FIR caption J1 (issue with reimbursement-service use). In-flight Refueling by Navy/Marine Corps Tankers.- The in-flight refueling operations are conducted by squadrons while deployed or NOT deployed. When NOT deployed, the material control officer of the transferring squadron is responsible for providing the local in-flight refueling form for the pilot to record the transactions. The form should contain the information needed to effect proper billing and reporting such as the unit identification code (UIC) of the receiving squadron. The custodian of the tanker aircraft is responsible for effecting the billing of all fuel delivered during in-flight refueling. The DD Form 1348 (6-pt) is used for documenting fuel transactions. The serial number of the document to be used for in-flight refueling will be Fill. The complete document number will include the following data: l Unit identification code (UIC) of the receiving squadron preceded by art R or V l Julian date and serial number with the date being the date when the tanker service is performed and serial number Fill l When feasible, include the aircraft bureau number of the aircraft that was refueled When it is necessary for the tanker to dump fuel while performing tanker service, regardless of the justification, the tanker squadron will absorb the cost. The squadron performing the tanker service must settle with the SAC 207 activity about the fuel received in conjunction with financial reporting. The tanker squadron must account for the total fuel received for squadron operations and total dispersed to other aircraft. For example, the total sum of fuel for the period is 10,000 gallons at $1.16 per gallon with the total being $11,600.00. The tanker squadron consumed 7,000 gallons for operations and 1,000 gallons each is dispersed to three other squadrons. It is necessary to prepare four separate DD Form 1348s (6-pt) to effect the settlement. The tanker squadron posts $8,120.00 to the OPTAR and each receiving squadrons posts $1,160.00 to their OPTAR. Table 6-3 lists how the documents are prepared for the transactions. During deployment, the pilot of the tanker squadron is responsible for filling out an in-flight refueling report after completing the mission. The material control officer of the tanker squadron is responsible for providing the local in-flight refueling form to the pilot. The carrier air wing commander is responsible for the

Table 6-3.-Tanker Squadron Fuel Documentation coordination of transactions between the tanker and recipient squadrons. The tanker squadron can obtain a credit for fuel by preparing a DD Form 1348 (6-pt) in the same manner as the DD Form 1348 prepared to load the tanker aircraft. The document number must also be the same except the quantity must be equal to the sum of fuel quantities transferred to other squadrons. The remarks block of the DD Form 1348 must contain the phrase J1 CREDIT. The in-flight refueling procedures also apply to squadrons using the Buddy Stores method of refueling. Fuel Received from the Air Force.- When fuel is obtained from the Air Force tanker aircraft, the receiving squadron will forward a DD Form 1348 (6-pt) to the tanker Air Force unit. The receiving squadron must request the tanker unit to maintain the document number and fund code in the Air Force billing document. Ensure the date of the refueling and the bureau number of the aircraft refueled are entered in the remarks block of the DD Form 1348 (6-pt). The address of the Air Force unit can be obtained in the DOD Activity Address Directory, DOD 4000.25-6-M, normally held at the supporting shore station or ship. Summarization of Transfers The value of material transfers and issues to other operating units and shore activities are summarized month] y. The summarization affects the necessary appropriation, subhead, operating budget, and cost accounting adjustments. The summarization does not include the Material Turned In to Store (MTIS) for credit. The mechaninized format or the Summary of Material Receipts/Expenditures, NAVCOMPT Form 176, is used to submit the report. The report is prepared and submitted to DAO on or before the 5th day of each month following the month in which the transactions were made. THE A SUMMARY.- This summary is used to effect funded (chargeable) adjustments between appropriations, subheads, and operating budgets. This also applies to adjustments between operating budgets within an appropriation and subhead. The A summary credit is applied to the type commander of the transferring activity by the DAO. THE FUEL A SUMMARY.- This summary is prepared monthly by the fleet commander only. This report is based on the information in the Navy Energy Usage Reporting System (NEURS) report that is submitted to the fleet commander. THE B SUMMARY.- This summary is used to effect statistical accounting adjustments (nonchargeable) between appropriation accounting classifications including adjustments between UICs. For example, transfer of DBOF material between activities under the same type commander will be included in the B summary and is nonchargeable. SUMMARY The duties and responsibilities of financial recordskeepers and supervisors aboard ships and ashore are vitally important. Personnel working with financial records must be familiar with the OPTAR, DBOF, and end-use accounting. The AK must learn the procedures for the different OPTARs. The TYCOM issues OPTARs for the operations and maintenance of the activity and for the flight operations (for aviation squadrons). Few AKs get involved with the OPTAR used for repair of other vessels (ROV). These OPTARs are administered and reported as prescribed for by the Financial Management of Resources Operating Pmcedures (Operating Forces), NAVSO P-3013. The DBOF is administered and reported as prescribed by various NAVSUP, NAVCOMPT, and DFAS-CL manuals. In this chapter, we discussed the basic principles, procedures, and verifications supervisors must know in financial management. We discussed the DB OF and OPTAR funds as separate entities and their relationships to each other. The list of terms and definitions will help you understand the procedures and reporting requirements in financial management. The flow of funds and budgeting procedures will give you an idea of how the activities get funded for required material and services. We discussed the symbols and codes used in appropriations, funds, and reports. You will become more familiar with these codes and symbols as you use them. We discussed the procedures used for managing the DBOF by SAC 207 activities. We also discussed the different FIRs carried in the SAC 207 and the reports generated by the DAO to reconcile the transactions that affect them. We described the different documents that will help you conduct the performance analysis in your activity. We discussed the procedures, required files, records and logs, and the responsibilities of personnel in maintaining the aviation squadron's OPTAR. As the material control supervisor or senior enlisted person in the squadron, you will be responsible for OPTAR maintenance. This chapter will help you understand your responsibilities to ensure that the OPTAR is properly used, documented, and reported. You should refer to the publications and manuals discussed in this chapter for the current information and procedures. |

|

|

|