Custom Search

|

|

|

||

|

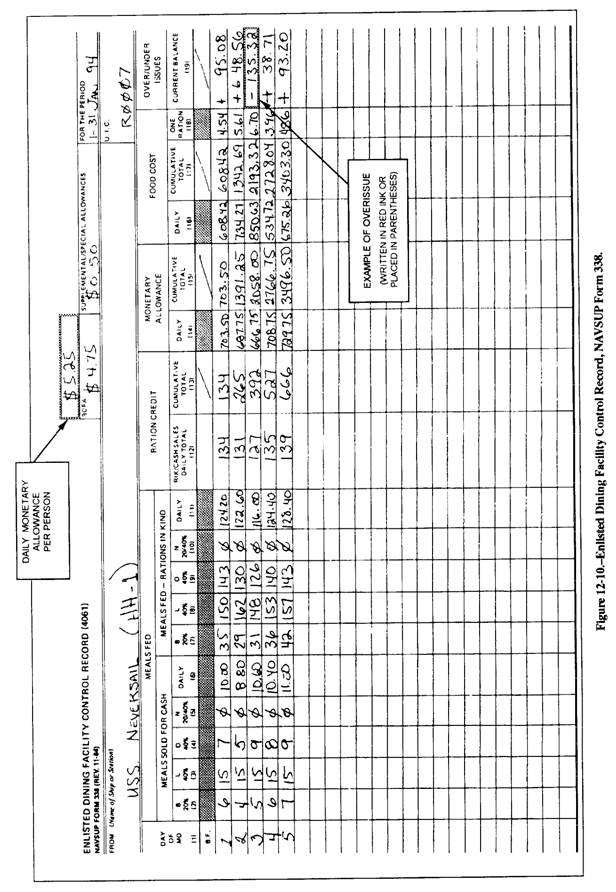

FOODSERVICE COST CONTROL GMs provide high-quality meals to authorized personnel. The FSO maintains financial accountability and control of the GM within the allowed monetary budget. Providing high-quality meals within a prescribed monetary allowance requires managerial skills and constant attention from the FSO and the foodservice division. As a junior MS, you learned the basics of a very challenging rating. As you advanced, your responsibility significantly increased and you now direct more and more of your attention to management. This incidentally is your rating's middle name. The key to effective management is control. As an MS third or second class petty officer, you learned the importance of portion control; also how it related to effective management on a smaller scale. We will now discuss the control procedures used to manage an effective operation and how to use the available resources and money to the Navy's best advantage. Navy GMs afloat and ashore operate on a monetary ration allowance. The allowances represent these dollars and cents called monetary rates. In 1933, the present Navy Ration Law, 10 U.S. Code 6082, came into effect. This law (specified in actual quantity of food) is a converted cash equivalency. You can compute this allowance by using the quantitative food allowance prescribed by the DOD Food Cost Index. This is based on food items authorized by the 1933 Navy Ration Law. The 1933 Navy Ration Law is listed by weight (such as 44 ounces of fresh vegetables) and converted to a monetary allowance. As a senior MS, you should understand not only what a ration is but also the various types of rations used in the Navy. Additionally, you should know which personnel are entitled to rations-in-kind, what forms to use in determining ration credit, and how to determine ration credit afloat and ashore. The NAVSUP P-486, volume 1, defines this in detail. One purpose of a cost control system in a mess is to provide you information on the financial operation of the mess. Cost controls provide the proper detailed information to give you the tools to overcome waste, lack of portion control, unwise menu planning, and/or pilferage; thus, ensuring guidance or restraint over money, material, and personnel. COMPONENTS OF FOOD COST CONTROL The following are five elements of cost control: 1. A prescribed operating limit or budget 2. A knowledge by management of the actions and procedures necessary to maintain within the prescribed operating limits of the mess 3. Prompt and accurate information on the daily progress toward maintaining within operating limits 4. The ability of management to rate the information received 5. The ability of management to follow up and take remedial action as necessary The financial requirements of each activity are subject to circumstances unique to the individual installation concerned. COMPUTING DAILY FOOD COST All GMs post total ration credits daily to the NAVSUP Form 338 whether ashore, afloat in port, or afloat at sea. The NAVSUP Form 338 is shown in figure -

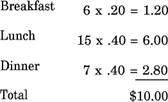

Ashore activities obtain ration credit information on meals sold and meals fed-rations-in-kind from the Subtotal line of the Recapitulation of Meal Record, NAVSUP Form 1292. Afloat activities enter the actual number of meals sold whether in port or at sea. These figures are obtained either from the Cash Meal Payment Book DD Form 1544, or the Sale of General Mess Meals, NAVSUP Form 1046. Meals fed rations-in-kind while at sea will be the same as the number of rations allowed daily. The actual head count numbers for each applicable meal will be used to reflect the number of meals fed rations-in-kind. The following information describes the procedures all GMs must use to complete columns (2) through (19) on the NAVSUP Form 338 ~: Columns (2) through (5). Enter the actual number of meals sold in the applicable column. Other meals, such as brunches, will be shown in the column applicable to directions that are provided in the most current NAVSUPINST 4061.9. Column(6). Multiply columns (2) through (5) by the applicable ration credit conversion factors for each meal. This conversion factor is shown at the top of each column. Carry the resulting figure out to two decimal places, then add the results and enter the total in column (6); for example:

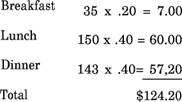

Column (11). Multiply rations-in-kind amounts in columns (7) through (10) by applicable ration credit conversion factors and then total these results; for example:

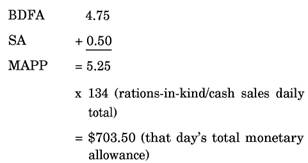

Column (12). Add the figure in column (6) to the figure in column (11). Then enter the results, rounded to the nearest whole number, in column (12). For example, 10.00 + 124.20= 134.20 is rounded off to 134. 0 Column (13). Add the figure in column (12) to the preceding day's entry in column (13). Then post the result in the current day's Cumulative Total column (13). Column (14). The monetary allowance per person (MAPP) is the amount of the basic daily food allowance (BDFA) and any supplemental or special allowance (SA). Multiply the number of rations in column (12) by the monetary allowance per person. Then post the result in column (14) as that day's total monetary allowance; for example:

Column (15). Add the figure in column (14) to the preceding day's entry in column (15). Then post the result in the current day's column Cumulative Total (15). Column (16). Total cost of rations for the day from the day's issues to the GM, less bakery products sold. Enter the resulting total in column (16). Column (17). Add the figure in column (16) to the preceding day's entry in column (17). Then post the result in the current day's column Cumulative Total (17). Column (18). Divide column (16) by column (12). Then post the result in column (18). Column (19). Subtract the figure in column (17) from the figure in column (15). Then post the result in column (19). Posting over- and underissues is described next. The over or under dollar value is the difference between cumulative food cost and cumulative monetary allowance. Column (17) is the cumulative food cost and column (15) is the cumulative monetary allowance. When the figure in column (15) is the greater, an underissue condition exists. This difference is posted in blue or black ink as a plus (+) sign in column (19). When the figure in column (17) is the greater, an overissue condition exists. This difference is posted in column (19) in either red ink preceded by a minus (-) sign or in blue or black ink enclosed in parentheses. |

|

|

|

||

|

|

Integrated Publishing, Inc. - A (SDVOSB) Service Disabled Veteran Owned Small Business

|