Custom Search

|

|

|

||

|

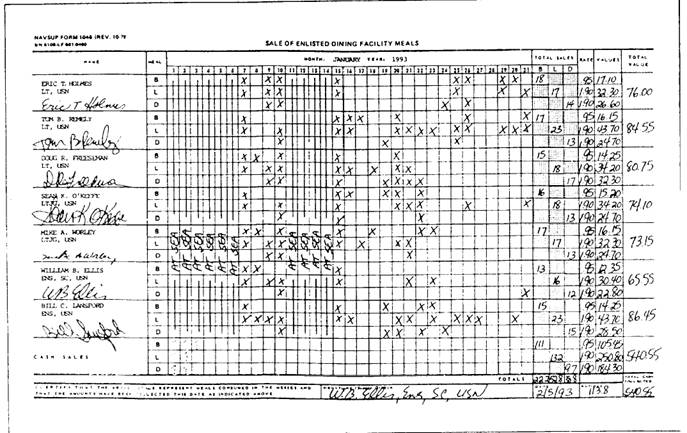

AUDITING ACCOUNTING RECORDS As was stated i~, the objective of any system of records maintained by a messing facility is to provide a source of data to be used in the preparation of the required financial statements for that messing facility. When properly maintained, these records also provide information that allows a more efficient operation of the messing facility. To this end it is vital that an auditing process be in place that allows for frequent checks of all records to ensure their accuracy. Balancing the Subsistence Ledger The records keeper maintains the Subsistence Ledger, NAVSUP Form 335, keeping one for each food item on board. This form provides a record by quantity of receipts and expenditures. It also provides a running balance on hand for each food item. Such transactions occur regularly and should be recorded to reflect the actual date of each transaction. The types of transactions are receipts, issues, sales, transfers, surveys, or inventory adjustments resulting from inaccurate inventory. Each transaction must be recorded accurately. To make sure all transactions are recorded accurately and the math is correct, the FSO or designated representative must periodically perform certain checks. He or she should check to make sure the correct unit is used for all transactions recorded. Unlike other stock items, food items have two unit prices-the fixed price and the last receipt price. The purchase price for food items on the commercial market fluctuates and the GM must operate on a fixed ration allowance. For this reason, NAVFSSO establishes a fixed price for all items used in the GM. Thus, the same charge is made for an item throughout the accounting period regardless of the current market or receipt price. The receipt price for each receipt should be entered in the space provided along with the date of receipt. This price is used to survey, transfer, or sell items to private messes and to extend inventory value. You can verify the current on-hand balance by adding all receipts to the opening inventory and subtracting all issues, transfers, surveys, and sales. The resulting figure should equal the current on-hand balance. You can confirm the Cumulative Total (issues) figure by running a printout or tape. Add the beginning inventory and all receipts. Subtract all quantities in the Other column and subtract the current on-hand balance. The result will equal the Cumulative Total figure if there are no mathematical errors on the NAVSUP Form 335. The Subsistence Ledger, NAVSUP Form 335, is considered a paper inventory and should not be interpreted as a true representation of the physical inventory. An actual physical inventory should be conducted to confirm the paper inventory. As was discussed earlier, frequent spot inventories should be conducted on fast-moving and high-cost items. The FSO is responsible for collecting required basic charges and surcharges received from the sale of meals from the GM. Additionally, he or she is responsible for depositing such funds with the disbursing officer. When wardroom members are furnished meals from the GM, whether continually or during in-port periods, the mess treasurer is responsible for the collection and reimbursement for such meals. RECEIPT AND RECORDING OF FUNDS.The FSO designates, in writing, cashiers to receive payment for all meals sold for cash. Payment may either be received in advance through sales of meal tickets or directly from personnel as they enter the GM. DOCUMENTATION.- Various forms are used to document sales of meals. Those used to classify ration entitlement and to document rations-in-kind were discussed earlier in the chapter. Discussed now are the forms used to record receipt of funds. Cash Meal Payment Book.- The Cash Meal Payment Book, DD Form 1544, is used to record meals sold for cash from a GM in the manner prescribed next. The CO will designate a control officer for the handling and security of the DD Form 1544. The transfer control and receipt coupons (four numbered coupons per book) will be used to complete the book. Individuals authorized to receive cash meal payment books sign the transfer control and receipt no. 1 at the time of receipt. The coupon is then retained by the control officer transferring the book. Another transfer control and receipt coupon is used to return the completed book. Cash Meal Payment Sheet Register.- The headings Organizations and Installation are filled in by the appointed control officer. The individual (normally a cashier) authorized to receive cash meal payment sheets should sign and insert the organization and date on the cash meal payment sheet register. He or she must make sure the sheet numbers correspond on both the payment sheets (described in the next paragraph) and the register. When the cash meal payment sheets are completed they are returned to the control officer. Now, the columns Date Returned, Cash Collected (foods surcharges), and Received By should be filled in. The Voucher No. column should not be completed since this column may be used at some future date. Cash Meal Payment Sheet.- Before using this form, the Organization block is completed. It also should have all applicable charges such as food charges, surcharges, or per diem as prescribed in the NAVSUPINST 4061.9. The cashier makes sure all individuals paying cash for meals sign their names and indicate their grade. He or she should then insert the applicable charge after each signature. A cash meal payment sheet also may be used for periods exceeding 1 day. In this case, the cashier should fill in the first unused line with his or her signature, rate, and date. Below this signature, rate, and date, a double line should be drawn to separate dates. After a payment sheet has been completed and all totals inserted, the cashier signs and inserts his or her rate and the date. The cashier then turns the sheet in to the control officer or appointed representative. When cash is turned in to a collection agent or disbursing officer, the DD Form 1544 serial and sheet numbers are entered next to the signature of the individual turning in the cash in the Cash Receipt Book, NAVSUP Form 470. The DD Form 1544 and the Sale of General Mess Meals, NAVSUP Form 1046 (credit sales), are used to substantiate sales from the GM and the ration credit claimed. The DD Form 1544 is audited and reconciled at the time the cash is collected by the collection agent or authorized custodian appointed to that established position by the FSO. The FSO should review the DD Form 1544 at least weekly and make sure an audit is made when the cash is collected. Funds held by the cashier more than the allowed change fund should be collected daily. The only exception to this is cash received from meals sold on weekends or holidays. This cash may be retained in the personal custody of the cashier provided adequate facilities exist for the security of such funds. Separate and adequate facilities should be either a secured safe with a three-tumbler combination lock or a locked container within a safe of this type. At the close of each meal period cashiers are personally responsible for the security of all funds in their possession. Cashiers remain responsible for such funds until depositing them with the authorized collection agent. The FSO appoints collection agents and authorized custodians. GM cashiers and the FSO cannot be designated as collection agents. Each individual responsible for funds must be provided with his or her own safe or a separate locked compartment in a larger safe. Overages and Shortages.- The cashier records overages and shortages in cash received from the sale of GM meals on the DD Form 1544. During the daily audit, the collection agent verifies the difference during the weekly DD Form 1544 inspection. The agent determines the cause of cumulative cash differences in excess of $1 or .05 percent (whichever is larger) per cashier for the week. The collection agent then acts as warranted by the circumstances to prevent a recurrence. Any cash discrepancy involving possible fraud or criminal act, regardless of value, should be recorded as outlined in the Navy Comptroller Manual. Total overages and shortages exceeding 10 dollars should be reported as part of line 5 on the NAVSUP Form 1357. This line is for undeposited sales that exist at the end of the month or patrol cycle. A letter should be prepared and submitted with the NAVSUP Form 1357 explaining the circumstances involved with the gain or loss. This letter also serves to request authority to reduce accountability by deposits (gains) or expenditures (losses) reported on line 5. Credit Sales.- If the sale of meals from the GM has been authorized and is considered quite practical, the CO may authorize the sale of meals on a credit basis. This authorization is for officers, enlisted, and other categories subsisting daily. When meals are sold on a credit basis, the Sale of General Mess Meals, NAVSUP Form 1046 ~, is used to record these credit sales in the following manner:

When the CO determines that it is impractical and uneconomical to subsist a small number of officers in the established wardroom during in-port periods, weekends, and holidays, he or she may authorize officers to purchase meals from the GM. At the option of the CO, a GM MS may be assigned the duty of maintaining the NAVSUP Form 1046. The MS should place a check mark or maintain a running total in the appropriate block opposite each name to show consumption of a meal. The form should be posted in a noticeable location where it can be seen by the wardroom mess members. At the end of each month, each mess member signs in the Name block to acknowledge approval of the meal tally. The payment for all meals sold on a credit basis is required no later than 15 days following the month in

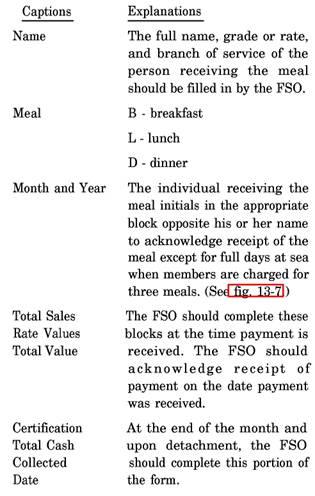

Figure 13-7.-Explanation of the Sale of General Mess Meals, NAVSUP Form 1046. which the meals were sold. Individuals concerned should make payment before detachment. The FSO furnishes a receipt for the cash paid. The Cash Receipt Certificate, NAVCOMPT Form 2114, maybe used as a receipt form. This is done by marking out the line "for which I hold myself accountable to the Treasurer of the United States of America." Deposit of Funds.- When practical, finds in excess of the change fund should be deposited daily with the disbursing officer. When impractical to make daily deposits, the cash should be deposited at least twice weekly. Any exceptions to this must be authorized by the Naval Supply Systems Command. When it is impractical for the collection agent to deposit cash daily, it should be retained in the collection agent's personal custody or turned in to the FSO. Accountability File The FSO must maintain files of accounting records and substantiating documents required for audit of subsistence, supply, and GM operations. Records and documents must be retained and disposed of according to Navy and Marine Corps Records Disposition Manual, SECNAVINST 5212.5. See also appendix B of the NAVSUP P-486, volume 1. RESPONSIBILITY.- The accountability file must be established by the FSO on the first day of the accounting period. SECURITY.-The accountability file must be kept under lock and key by the accountable officer to maintain security of all accountable transactions and substantiating accountable documents. At the end of the quarter, the documents in this file become the ship's retained returns for the period, except the rough inventory. The rough inventory should be retained in the accountability file until the next rough inventory is made. |

||

|

||