|

||

|

|

||

|

Page Title:

Review by the Ship's Store Officer |

||

| |||||||||||||||

|

|

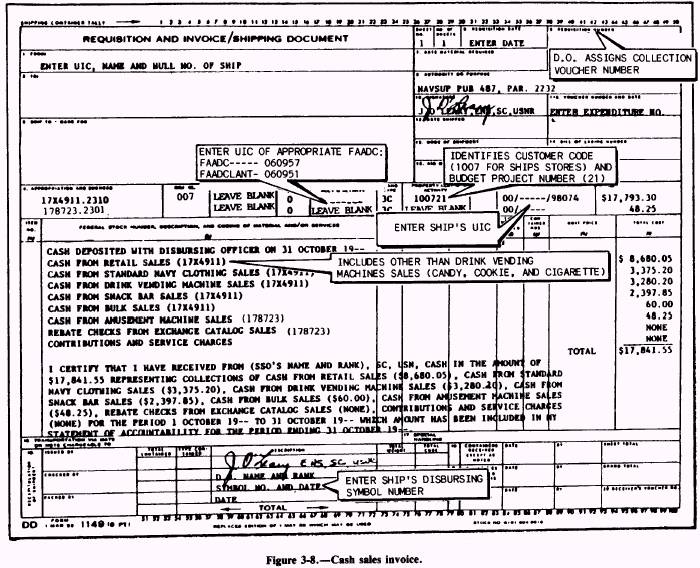

REVIEW BY THE SHIP'S STORE OFFICER As the collection agent, you will submit the following records to the ship's store officer when making collections on a daily basis or a minimum of twice a week: The Cash Register Record, NAVSUP Form 469, for each sales outlet The Cash Receipt Book, NAVSUP Form 470, for each sales outlet The Cash Receipt Book, NAVSUP Form 470, covering deposits with the disbursing officer The ship's store officer reviews all entries, checks amounts deposited with the disbursing officer, and initials all entries in both the NAVSUP Forms 469 and 470 to indicate they have been checked. In ROM operations, the ship's store officer will additionally check to make sure cash collections are entered correctly. CASH SALES INVOICE A memorandum cash sales invoice deposit of cash with the disbursing officer (DD Form 1149) is prepared monthly to substantiate cash receipts from sales. It is also prepared when the ship's store officer or disbursing officer is relieved, or when cash is deposited with a different disbursing officer. Any time a cash sales invoice is prepared, the ship's store officer verifies the NAVSUP Forms 469 and 470 to make sure figures on the cash sales invoice match with the figures on the NAVSUP Forms 469 and 470 and the figures entered in the ROM system. The cash sales invoice is normally prepared by the ship's store recordskeeper for signing by the disbursing officer. In ROM operations, the ROM system automatically totals cash collections and will print the DD Form 1149 when required. In manual records after the NAVSUP Form 469 is balanced and closed out for all sales outlets, the collection agent forwards all information to the sales office for preparation of the cash sales invoice. Figure 3-8 is an example of a cash sales invoice. Look at the figure and study each entry. The amount of cash from retail sales includes cash collected for the month from retail stores and vending machines other than drink vending machines such as candy, cookie, and cigarette. When standard Navy clothing is sold through the same register as ship's store stock, and the cash register does not have departmental keys, the retail sales figure for the first 3 months of the accounting period will include standard Navy clothing sales. At the end of the accounting period, an inventory is taken of all standard Navy clothing. The total inventory is included on the Journal of Expenditures, NAVSUP Form 978, and the cost of standard Navy clothing sales will be forced in closing out the NAVSUP Form 978. Enter this force figure as cash from standard Navy clothing sales on the cash sales invoice, DD Form 1149, for the final month of the accounting period. The ROM system will automatically compute standard Navy clothing sales at the end of the accounting period based on the inventory of all department code L-1 items entered. ROM will post all records that apply and adjust the sales figure on the DD Form 1149. If the sales of standard Navy clothing are through a register separate from sales received from ship's store stock, then enter the cash collected from standard Navy clothing sales each month of the accounting period. Cash collected from drink vending machine sales is the actual cash collected from drink vending machine sales. Cash from snack bar sales is the cash collected from snack bar sales including retail and manufactured items. Cash from bulk sales is the total cash collected from bulk sales. Cash collected from amusement machines includes all cash collected from amusement machines. Rebate checks from exchange catalog sales include the total amount of all rebate checks received from the Navy Resale and Services Support Office for exchange catalog sales. Contributions and service charges include the total amount of funds received from contributions to ship's store profits, including service charges collected and profits from sales of traveler's checks. COMMON CASH COLLECTION ERRORS Most errors made in cash collection are due to using improper cash collection procedures. Since the cash and receipts must always balance, there is no room for errors in cash collection. The Navy audit service recently did an audit of ship's store afloat. It was discovered that cash collection agents did not properly collect and record all cash from retail sales, amusement machines, vending machines, and change machines. Cash collections were not made daily, posted to the cash register record, or verified by the ship's store officer. The following are common errors made in cash collection: l Cash is not collected at the end of each business day except as authorized in the NAVSUP P-487. . All cash including change fund is not collected from the retail store or snackbar when it will be closed for a period of more than 72 hours. l A Cash Receipt Book, NAVSUP Form 470, is not maintained for every sales outlet,

3-17 Figure 3-8. . Entries are not closed out or compared on the Cash Register Record, NAVSUP Form 469, and the Cash Receipt Book, NAVSUP Form 470, with the Cash Sales Invoice. . Cash collections from the sales outlets are not properly safeguarded by keeping them in a secure safe. l Cash register tapes removed from the register are not signed, dated, or filed. . Overring or refund vouchers are not recorded properly in the Cash Receipt Book, NAVSUP Form 470, or Cash Register Record, NAVSUP Form 469. . Collections are not deposited with the disbursing officer daily. l Register readings are not being taken. . Sales outlet operator is not present during collection and counting of monies. . Cash from group sales is collected directly by the cash collection agent and not rung up on the register first. . Change funds are issued without receiving a receipt. . Shortages or overages noted in the Cash Register Record, NAVSUP Form 469, were not initialed by the ship's store officer when in excess of $5. . Ship's store officers did not review the cashbooks a minimum of twice weekly when the collection agent was making collections. . Overring/Refund Vouchers, NAVSUP Form 972, are not filled out properly or approved by the ship's store officer. . Cash collection figures entered in the ROM are not compared with the total cash collected as reported on the NAVSUP Form 469 and NAVSUP Form 470. The list of errors is many; however, the use of procedures outlined in the NAVSUP P-487 will eliminate every problem above. Not only should you improve your knowledge of cash collection, but you should also make sure the sales outlet operators you collect from thoroughly understand collection procedures. In the long run, better supervision and training will improve internal controls for handling cash collections. This information is now available on CD in Adobe PDF Printable Format |

|

Privacy Statement - Press Release - Copyright Information. - Contact Us - Support Integrated Publishing |

|

|

Integrated Publishing, Inc. - A (SDVOSB) Service Disabled Veteran Owned Small Business

|