Custom Search

|

|

|

||

|

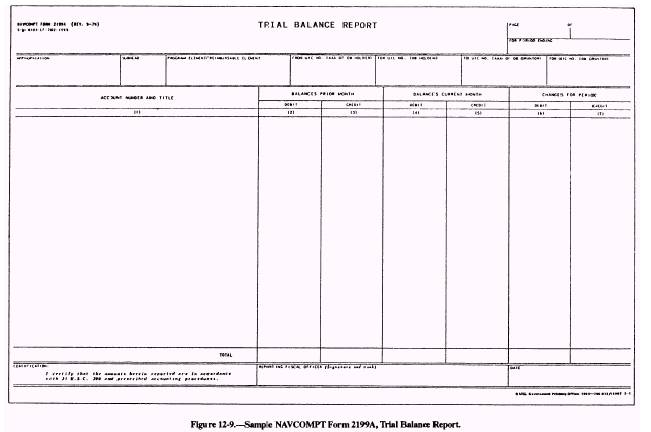

The primary report used to manage these funds is the Trial Balance Report, NAVCOMPT Form 2199A (fig. 12-9). This report must be reviewed to verify that the amount of funds authorized is accurately recorded on the report. To do this, compare your current authorization to the amount shown for the General Ledger Account (GLA) 1031. They should be equal. The amount currently reported as obligations in the GLA 0998 should be reviewed next. This figure should be as current as possible. If you are able to enter your obligations directly into the system, this should not be a problem. Next, review what has been disbursed by looking at the GLA 1060. Within several months after the end of each fiscal year, this should equal the total amount obligated. If this is not the case, determine the reasons for the differences. Finally, determine if there were any problems in liquidating the amounts obligated by looking at the GLA 1960. This will tell you what amounts have been disbursed against your account that have problems (for example, no corresponding obligation or erroneous accounting data). Make sure these problems are promptly corrected. Your responsibilities do not end on 30 September. You must continue to review NAVCOMPT Form 2199A for prior years to make sure the obligations are promptly liquidated and erroneous expenditures are not charged against your operating budget. RECONCILIATION Reconciliation compares what is recorded in your memorandum accounting logbook with what has been recorded in the accounting system. You must reconcile both obligations and expenditures. What makes reconciliation so crucial is that the authorization accounting activity (AAA) records are the official records accepted by higher authority. For this reason they must be correct. Although the responsibility for the error may not be yours, the responsibility for an overobligation is yours. his is why you are responsible for reconciliation, not the AAA. To reconcile you must understand what happens to a voucher after it has been prepared. The original and copies are sent to the disbursing office. A copy is retained in the preparing office for its records and either (1) a copy is sent to the AAA or financial information processing center (FIPC) to record the obligations or (2) an obligation entry is made using your local AAA/FIPC automated system. The Navy Comptroller Manual states that an approved claim authorized by law is an obligation. Therefore, to maintain current obligations, the AAA/FIPC must receive and obligate advance copies of payment vouchers. Then, when a copy of the paid voucher is received from the disbursing officer, the claim payment is removed from the accounts payable and becomes classified as an expenditure. Occasionally an AAA may not receive an advance copy of a payment voucher. In those rare instances, the AAA would have an immediate expenditure. At the end of each month, the AAA uses these entries to generate several accounting reports. One of these reports is the NAVCOMPT Form 2199A. This report gives cumulative figures for your claims authorization. If the cumulative obligtitions shown on the NAVCOMPT Form 2199A equal the cumulative amounts recorded in the memorandum accounting logbook, then they are in balance and reconciliation should normally be the case. Reconcile by job order, First verify that the amount obligated in the job order is accurately reported. Then check the listing of unliquidated obligations to see what obligations have not yet been liquidated. To reconcile, you need two reports from your AAA-a listing of expenditures processed against your authorization and a listing of all outstanding obligations. If you have not received the necessary reports from your AAA and the AAA will not cooperate, JAG should be advised. The AAA is responsible for cooperating in any way possible and responding to any reasonable requests.

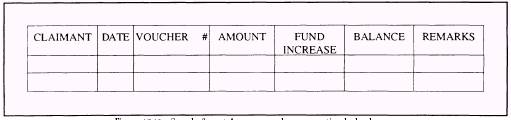

The two reports discussed previously are the Accounts recorded in the accounting system that are incorrect-both obligations and expenditures Canceled vouchers or vouchers improperly charged against a job order that are recorded in the accounting system-both obligations and expenditures Report all errors to the appropriate person at your accounting activity. NOTE: If you have access to an Integrated Disbursing and Accounting System terminal, you will be able to directly enter the obligations yourself. This should make reconciliation easier especially if you enter them in a timely manner. You may also receive a weekly transaction listing. Although this enables a weekly reconcilitition, a monthly reconciliation is adequate-except at the end of the fiscal year when it is critical that fund status be closely monitored. The key to effective accounting is a good UNLIQUIDATED OBLIGATIONS You are not done managing Navy claims funds until MEMORANDUM ACCOUNTING LOGBOOK A sample format for the memorandum accounting logbook is shown in figure 12-10.

Figure 12-10.-Sample format for memorandum accounting logbook page. sent out in batches, always run a new total after each batch is sent out. This will facilitate reconciliation if the accounting activity has not recorded the last batches forwarded in the month, then you will need only to look through the memorandum accounting logbook for the last batch recorded for use as the point of reconciliation. NOTE: The accounting activity can establish a cutoff date as to the last day in the month that documents can be forwarded to them for posting. This is to make sure all documents forwarded before that date will be posted on the report for that month. If you do not enter the obligations yourself, it is usually a good policy to stop sending vouchers to the accounting activity 3 working days before the end of the month. Of course this policy does not apply at the end of the fiscal year, when the allottee must coordinate with the AAA to make sure all obligations have been received and posted. |

|

|

|

||