Custom Search

|

|

|

|

|

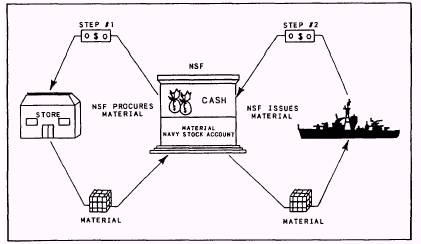

The duties and responsibilities of the financial recordkeeper are vitally important, especially at Shipboard Uniform Automated Data Processing System-Real Time (SUADPS-RT) activities. The financial recordkeeper must perform both OP-TAR accounting and Navy Stock Fund (NSF) accounting. TYCOMs issue separate OPTARs for the operation and maintenance of the activity, for the repair of other vessels, and for flight operations. These OPTARs are administered and reported by the Financial Management of Resources Operating Procedures (Operating Forces), NAVSO P-3013-2. The NSF is administered and reported as prescribed by various Naval Supply Systems Command (NAVSUP) and NAVCOMPT manuals. The financial recordkeeper must recognize that the OPTAR funds are separate from the NSF. However, there is a relationship between these two funds that must be understood. NAVY STOCK FUND The NSF is a revolving fund established by Congress to purchase material carried in stock ashore as inventory by the Navy stock points and material carried afloat by destroyer tenders (ADs),

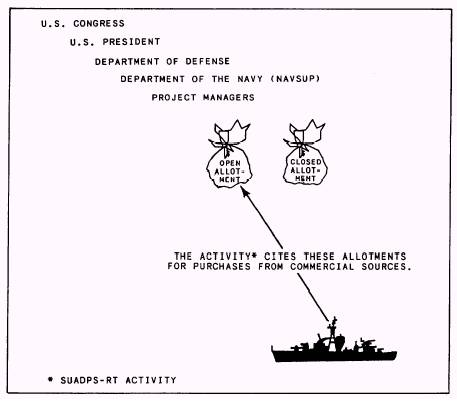

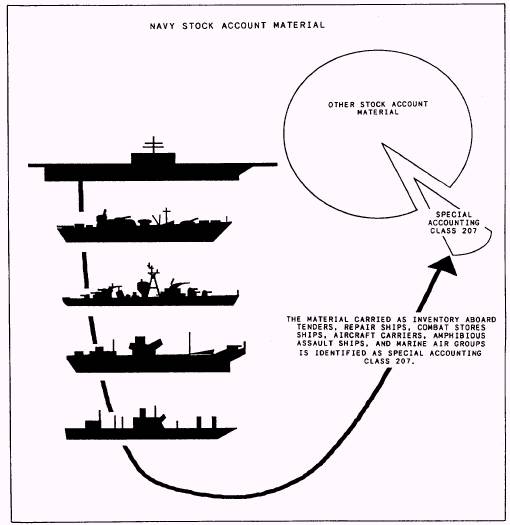

Figure 2-2.-The Navy Stock Fund (a revolving fund). repair tenders (ASs), combat stores ships (AFs), aircraft carriers (CVs), nuclear-powered carriers (CVNs), amphibious assault ships (LPHs), helicopter assault landing ships (LHAs), and marine air groups (MAGs). These activities spend NSF dollars to procure items expended to art enduse customer. The fund is reimbursed when material is requisitioned for use by charging the customer's OPTAR and crediting the NSF. This transaction returns the money to the NSF so replacement material may be purchased and the revolving fund continued, as shown in figure 2-2. The amount of the NSF is determined by Congress and, when approved, is passed down through the chain of command to the Department of the Navy, as shown in figure 2-3. Within the Department of the Navy, the Naval Supply Systems Command (NAVSUPSYSCOM) is responsible for the overall administration of the NSF. For accountability, material procured with Navy Stock Account (NSA) money is classified as NSA material, and activities that stock this material are called NSA activities. The primary mission of afloat units such as tenders, repair ships, and combat stores ships is repair and/or supply support. Although the primary mission of aircraft carriers, amphibious assault ships, and MAGs is combat, they also are assigned a supply support function. Therefore, these activities are considered intermediate supply facilities and are authorized to carry NSA material as inventory. Material carried in inventory aboard these activities is in special accounting class (SAC) 207

Figure 2-3.-Distribution of the Navy Stock Fund. to differentiate it from NSA material at other stock points as shown in figure 2-4. SPECIAL ACCOUNTING CLASS 207 TRANSACTIONS When SUADPS-RT activities requisition material for stock or direct turnover (DTO), they use NSF money by citing the SAC 207 fund code on the external requisition. When the material is received, it is recorded as a receipt in the NSA. When this material is issued to departments for use, OPTAR funds are used to reimburse the NSF. This is done by citing the activity's unit identification code (UIC) and the TYCOM's fund code on the issue document, resulting in a charge to the OPTAR fund and a reimbursement to the NSF. For DTO receipts, the SUADPS-RT computer processes the receipt into the SAC 207 fund and generates a charge to the end user's OPTAR fund.

Figure 2-4.-Navy Stock Account and SAC 207. 2-6 |

|

|

|