Custom Search

|

|

|

|

|

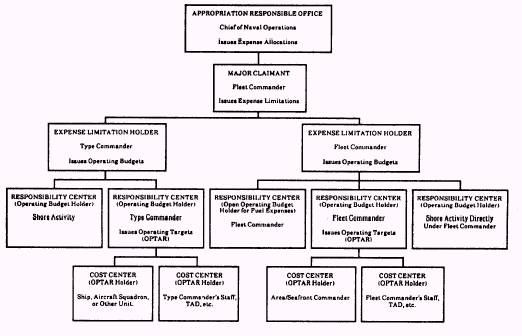

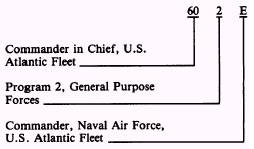

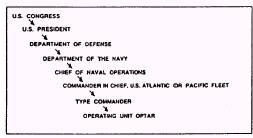

FLOW OF FUNDS It is a policy of the Secretary of the Navy (SECNAV) that the accounting effort performed by Navy Operating Forces be kept to the absolute minimum. The responsibility y for formal accounting is to be placed ashore. All material and services requisitioned by a Navy squadron ultimately cost the U.S. Government money. Since the requirement for these items originates in the squadron, it follows that financial responsibility starts there as well, The next higher level of financial responsibility is the aircraft controlling custodian (ACC) or TYCOM (fig. 2-5). The AK2 does not get involved with funding above the ACC or TYCOM level. Therefore, for the purposes of this TRAMAN, a discussion of funding is limited to the ACC or TYCOM and the cost center. FLEET ACCOUNTING AND DISBURSING CENTER MANAGEMENT REPORTS The fleet accounting and disbursing centers (FAADCs) perform the official accounting and reporting for OPTARs issued by the TYCOM. The FAADCs establish the necessary controls to maintain and prove the accuracy and propriety of transactions. These controls include the required document files and related accounting records. The FAADCs maintain records of each obligation document and, as requisitioned material is supplied and vouchers paid, match them to the expenditure documents received from the supply activities and disbursing office. The result is reported to the ship or squadron by listings prepared on data processing equipment. The listings allow OPTAR AKs to make necessary corrections to the appropriate records and to report any errors to the FAADC. To help in the proper accounting of fleet funds held by the individual OPTAR holders, the FAADCs, U.S. Atlantic Fleet (FAADC-LANT) and U.S. Pacific Fleet (FAADCPAC), periodically submit several transaction listings to the fleet units for review, validation, or correction.

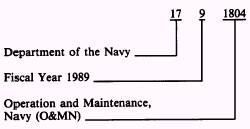

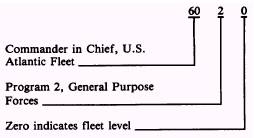

Figure 2-5.-Flow of funds for Operations and Maintenance, Navy. 2-7 The fund identification system is broken down into several elements. These elements are discussed in the following paragraphs. Appropriation Symbol An appropriation symbol consists of a sevendigit number identifying the government agency responsible for administering the appropriation, the fiscal year, and the specific appropriation. Table 2-1 is an example of an appropriation symbol. Subhead Symbol The four-digit subhead symbol for the O&MN appropriation identifies the major program of the Five-Year Defense Plan (FYDP). The first two digits represent the last two digits of the major claimant's UIC. The third digit identifies the major program or budget activity of the FYDP. The fourth digit is a zero at the major claimant (fleet) level. Table 2-2 is an example of a subhead symbol. An expense limitation cites the same subhead from which it is issued, except that the fourth digit is an alphabetic or numeric character by the major claimant to identify the expense limitation holder. Table 2-3 is an example of an expense limitation subhead symbol. The term operating target (OPTAR) is defined as an estimate of the amount of money that will

Table 2-1.-Appropriation Symbol

Table 2-2.-Subhead Symbol be required by an operating ship, staff, squadron, or other unit to perform assigned tasks and functions. Each year Congress enacts an O&MN appropriation that authorizes the Navy to buy needed material and services. A portion of this appropriation is passed down through the chain of command to the activity in the form of an OPTAR grant. As shown in figure 2-6, SUADPS-RT activities receive OP-TAR grants from the TYCOMs. The number and type of OPTAR grants provided these activities depend on the mission of the activity. All SUADPS-RT activities (except MAGs) receive supplies and equipage (S&E) OPTAR grants to cover the operation and maintenance of the activity. They may also receive a reimbursable OPTAR when a requirement exists to provide work or services to another TYCOM or government department as directed by the activity's TYCOM. Tenders and repair ships receive repair of other vessels OP-TARs to finance the material or services used in the repair of other ships. Aircraft carriers, amphibious assault ships, and MAGs receive

Table 2-3.-Expense Limitation Subhead Symbol

Figure 2-6.-Distribution of OPTAR funds. aviation fleet maintenance (AFM) OPTARs to cover the cost of aircraft maintenance. Aviation squadrons receive flight operations (FLTOPs) OPTARs to cover the cost of flight operations maintenance. To determine the authorized charges to each of the above mentioned OPTARs, refer to NAVSO P-3013. Procedures for the accounting of an activity's OPTAR are explained in detail in Financial Management of Resources (Operating Forces.), NAVSO P-3013; Automated Snap I Supply Procedures, volume 2; and SUADPS-RT Support Procedures, Financial Management Subsystem, volume III. All these publications are important background References for AKs involved in OP-TAR accounting. |

|

|

|