|

||

|

|

||

|

Page Title:

Can Drink Vending Machines Entry |

||

| |||||||||||||||

|

|

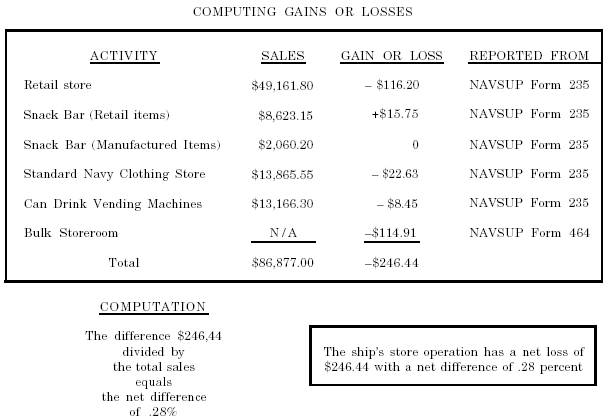

Can Drink Vending Machines Entry For the can drink vending machines, enter the dollar amount of the overage or shortage reported on the difference line followed by the percentage of the overage or shortage. The ROM system automatically posts difference information. Below the percentage of the overage or shortage, enter the cost of sales. The cost of sales is the amount shown on line R of ALL Vending Machine Controls, NAVSUP Form 236, for the accounting period. Look at figure 6-12 as we use the following formula to compute the gross profit: Amount shown on the sales line. . . . $13,166.30 minus Amount reported on cost of sales line . . . . . . . . . . . . . . . . . . . . . . . . . . $8,275.96 equals Gross profit . . . . . . . . . . . . . . . . . . . . $4,890.34 $13,166.30 - $8,275.96 = $4,890.34 Once you figure the gross profit, compute the percentage of gross profit by dividing the amount of gross profit by the amount on the sales line. In our example, $4,890.34 divided by $13,166.30 equals a gross profit percentage of 37 percent. The ROM system automatically posts this information. Cup-Type Drink Vending Machines Entry For cup-type vending machines (fig. 6-12), enter the cost of sales which equals the amount reported on the sales line ($2,300) minus the amount reported on the difference line ($1,337.20). The cost of sales in this case would be $962.80. Below the cost of sales, enter the gross profit. The gross profit is the amount reported on the difference line of $1,337.20. Then enter the percentage of gross profit by dividing the gross profit of $1,337.20 by the amount on the sales line of $2,300 to give you gross profit of 58 percent. The ROM system automatically computes this information. Other Than Drink Vending Machines Entry For other than drink vending machines, enter the amount of overage or shortage reported on the difference line followed by the percentage of overage or shortage. This is computed automatically by the ROM system. Snack Bar Retail Items Entry For snack bar retail items, enter the amount of overage or shortage reported on the difference line followed by the percentage of overage or shortage. The ROM system automatically computes difference information. Snack Bar Manufactured Items Entry For snack bar manufactured items, enter the gross profit amount reported on the difference line followed by the percentage of gross profit. To compute the percentage of gross profit, divide the gross profit by the amount reported on the sales line. Cost of Operation Entry For the cost of operation material, enter the value of all items issued from the Cost of Operation column except for issues to the drink vending machines. For cost of operation vending machines, enter the total value of all items for the vending machines from the Cost of Operation column. GAINS OR LOSSES Once you complete inventory and closeout, the NAVSUP Form 235 and the NAVSUP Form 464 gains or losses are identified. The amount of those gains or losses is a difference compared to the total sales for an individual outlet or the total sales for all outlets. The amount or percentage of difference determines what course of action the ship's store officer must take. Determine the percent of difference for the entire ship's store operation using the formula shown in figure 6-13. In the example, the total difference of all sales outlets including the bulk storeroom is $246.44, the total net loss. The figures for the differences of each individual sales outlets are obtained from the Ship's Store Afloat Financial Control Record, NAVSUP Form 235, and the figures for the differences of the bulk storeroom are obtained from the discrepancy list. The total net loss of $246.44 is then divided by the total sales for all the sales outlets of $86,877 for the net difference of .28 percent. Once you determine the net difference, then determine if it is within monetary limits. An excessive difference exists when the total inventory dollar value difference between the financial control records and the physical inventory exceeds $750 or 1 percent of total sales, whichever is greater. If this is the case, then the ship's store operation is not within monetary limits and action must be taken. ACTIONS TAKEN FOR EXCESSIVE DIFFERENCES When an excessive difference is discovered during records closeout, the supply officer must be notified and all ship's store accountable spaces are secured and numbered car seals placed on them until the difference can be resolved.

Figure 6-13.-Computing gains and losses. 6-23 The first step taken to resolve the difference is an attempt to take care of the shortage or overage at a divisional level. This is done by verifying all mathematical computations on the records and using the checkoff list in the NAVSUP P-487, par. 9102, that indicates the most common discrepancies that occur. If this does not resolve the problem, then the commanding officer must be notified. The commanding officer initiates an informal examination of the loss that includes rechecking the most common errors shown in the NAVSUP P-487 and determining the total dollar value of the difference based on inventory and financial control records closeout. If this informal investigation determines there is no excessive loss, no further action is required. If the excessive difference is not resolved, the following actions are taken: . Assistance is requested from the TYCOM or local NAVRESSO fleet assistance team. . Accountability is reestablished and spaces are reopened for business. l Disciplinary action is taken according to the UCMJ, if required. . If theft or fraud is discovered, the instructions in the NAVSUP P-487, par. 1206 (2) and (3), are followed. This information is now available on CD in Adobe PDF Printable Format |

|

Privacy Statement - Press Release - Copyright Information. - Contact Us - Support Integrated Publishing |